Introduction to Chart of Accounts

A chart of accounts is a listing of the names of the accounts that a company has identified and made available for recording transactions in its general ledger. A company has the flexibility to tailor its chart of accounts to best suit its needs, including adding accounts as needed.

Within the chart of accounts you will find that the accounts are typically listed in the following order:

Within the categories of operating revenues and operating expenses, accounts might be further organized by business function (such as producing, selling, administrative, financing) and/or by company divisions, product lines, etc.

A company’s organization chart can serve as the outline for its accounting chart of accounts. For example, if a company divides its business into ten departments (production, marketing, human resources, etc.), each department will likely be accountable for its own expenses (salaries, supplies, phone, etc.). Each department will have its own phone expense account, its own salaries expense, etc.

A chart of accounts will likely be as large and as complex as the company itself. An international corporation with several divisions may need thousands of accounts, whereas a small local retailer may need as few as one hundred accounts.

Sample Chart of Accounts For a Large Corporation

Each account in the chart of accounts is typically assigned a name and a unique number by which it can be identified. (Software for some small businesses may not require account numbers.) Account numbers are often five or more digits in length with each digit representing a division of the company, the department, the type of account, etc.

As you will see, the first digit might signify if the account is an asset, liability, etc. For example, if the first digit is a “1” it is an asset. If the first digit is a “5” it is an operating expense.

A gap between account numbers allows for adding accounts in the future. The following is a partial listing of a sample chart of accounts.

- Current Assets (account numbers 10000 – 16999)

- 10100 Cash – Regular Checking

10200 Cash – Payroll Checking

10600 Petty Cash Fund

12100 Accounts Receivable

12500 Allowance for Doubtful Accounts

13100 Inventory

14100 Supplies

15300 Prepaid Insurance - Property, Plant, and Equipment (account numbers 17000 – 18999)

- 17000 Land

17100 Buildings

17300 Equipment

17800 Vehicles

18100 Accumulated Depreciation – Buildings

18300 Accumulated Depreciation – Equipment

18800 Accumulated Depreciation – Vehicles - Current Liabilities (account numbers 20020 – 24999)

- 20120 Notes Payable – Credit Line #1

20220 Notes Payable – Credit Line #2

21000 Accounts Payable

22100 Wages Payable

23100 Interest Payable

24500 Unearned Revenues - Long-term Liabilities (account numbers 25000 – 26999)

- 25100 Mortgage Loan Payable

25600 Bonds Payable

25650 Discount on Bonds Payable - Stockholders’ Equity (account numbers 27000 – 29999)

- 27100 Common Stock, No Par

27500 Retained Earnings

29500 Treasury Stock - Operating Revenues (account numbers 30000 – 39999)

- 31010 Sales – Division #1, Product Line 010

31022 Sales – Division #1, Product Line 022

32017 Sales – Division #2, Product Line 015

33110 Sales – Division #3, Product Line 110 - Cost of Goods Sold (account numbers 40000 – 49999)

- 41010 COGS – Division #1, Product Line 010

41022 COGS – Division #1, Product Line 022

42017 COGS – Division #2, Product Line 015

43110 COGS – Division #3, Product Line 110 - Marketing Expenses (account numbers 50000 – 50999)

- 50100 Marketing Dept. Salaries

50150 Marketing Dept. Payroll Taxes

50200 Marketing Dept. Supplies

50600 Marketing Dept. Telephone - Payroll Dept. Expenses (account numbers 59000 – 59999)

- 59100 Payroll Dept. Salaries

59150 Payroll Dept. Payroll Taxes

59200 Payroll Dept. Supplies

59600 Payroll Dept. Telephone - Other (account numbers 90000 – 99999)

- 91800 Gain on Sale of Assets

96100 Loss on Sale of Assets

Sample Chart of Accounts for a Small Company

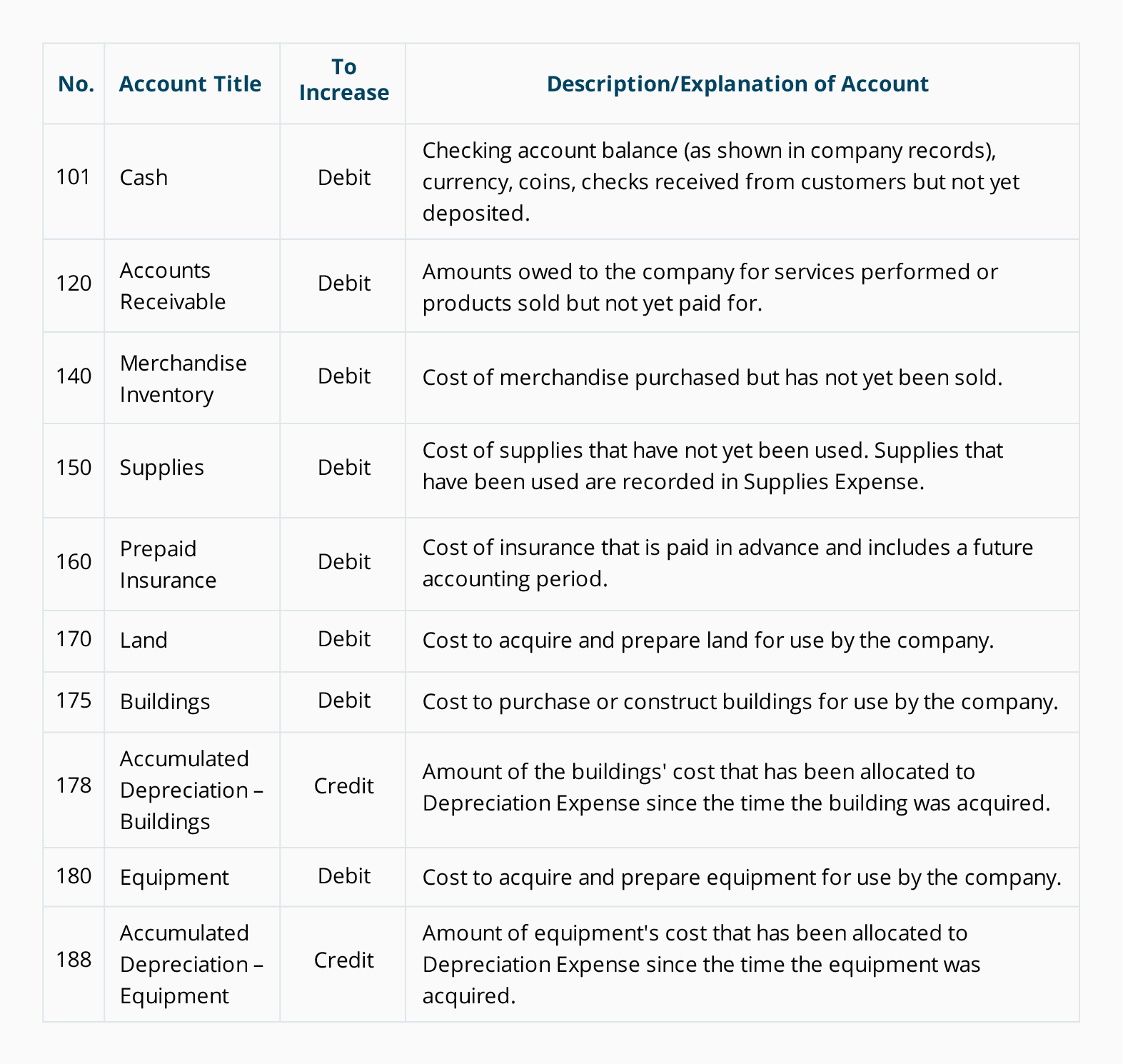

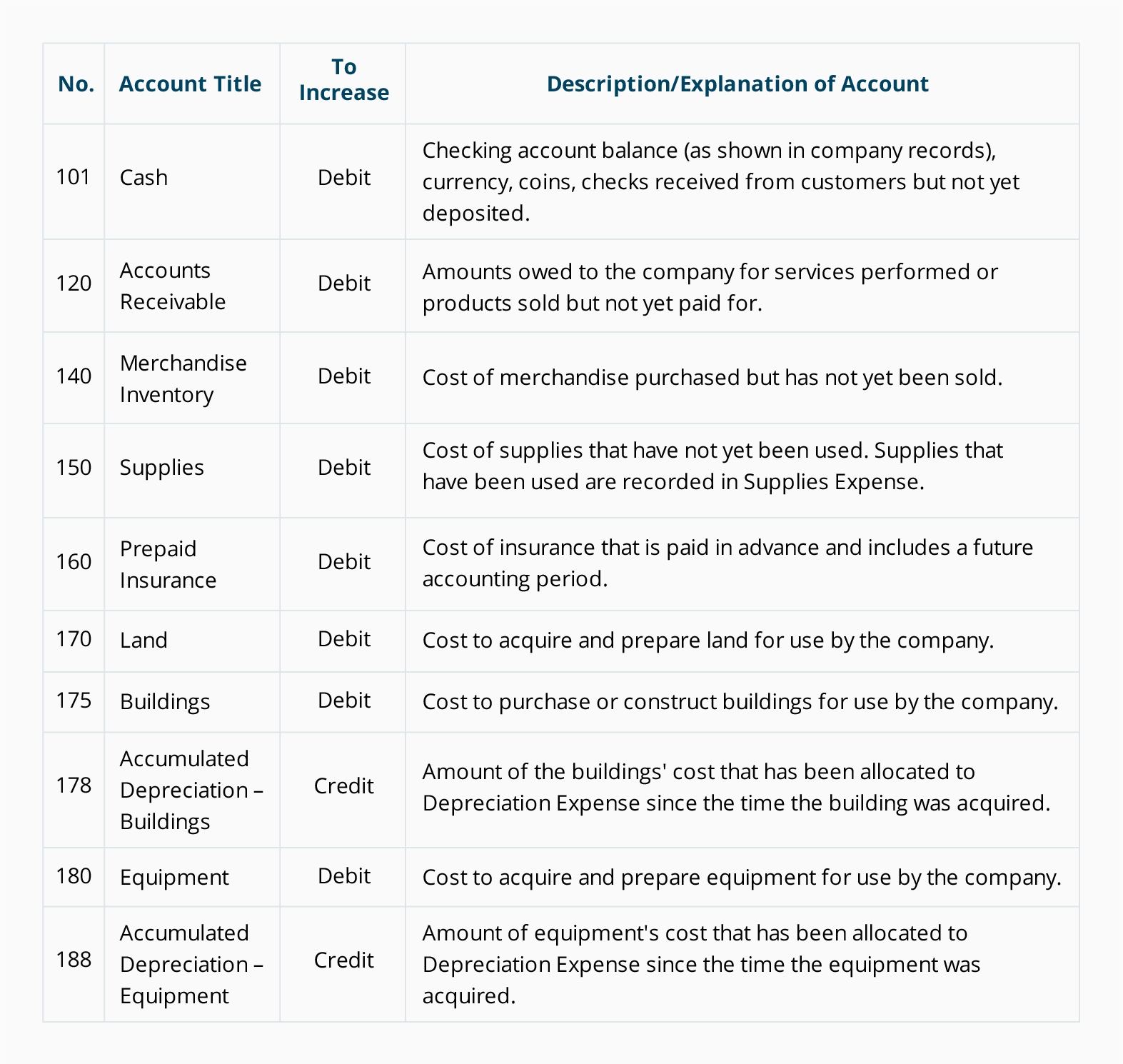

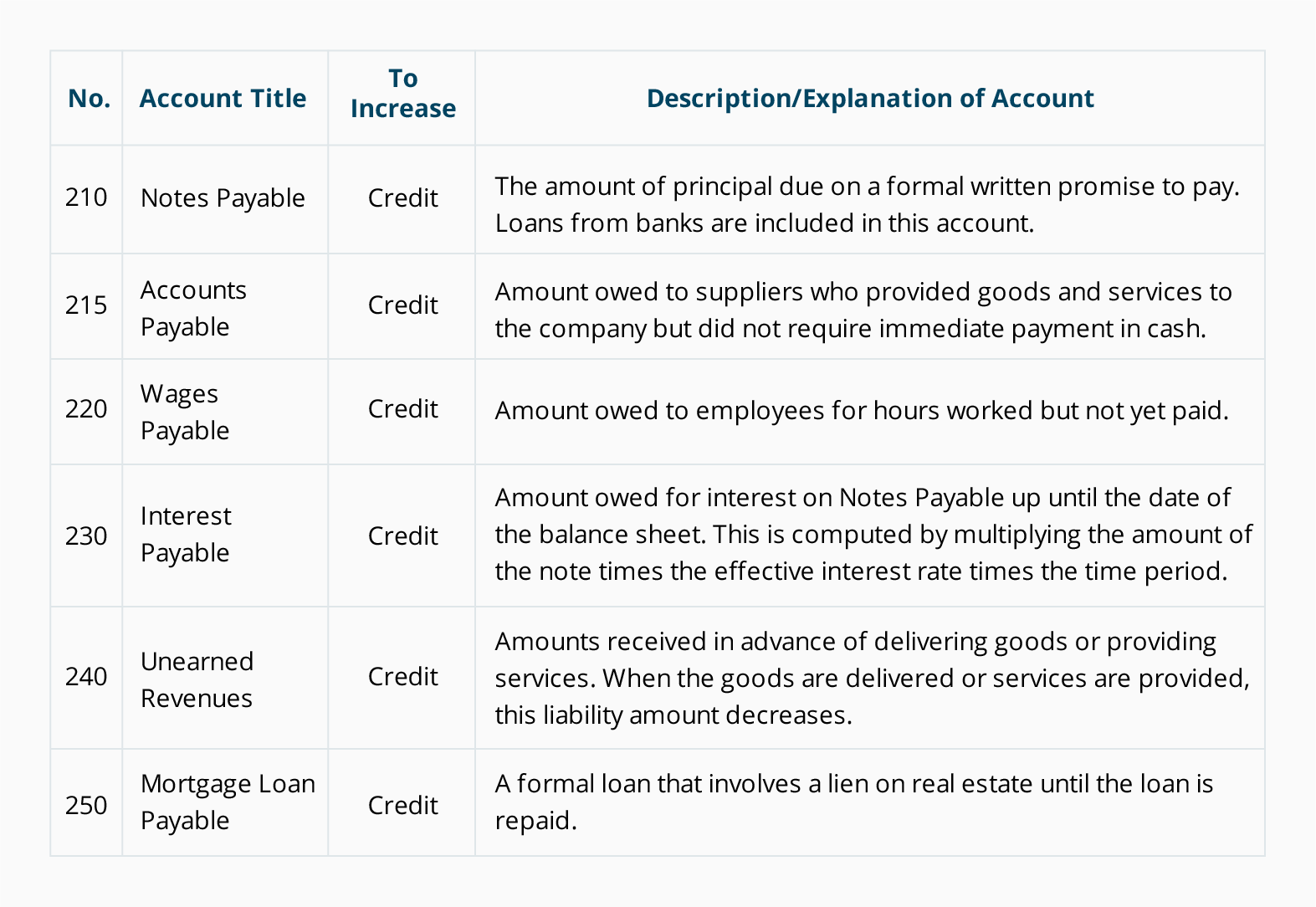

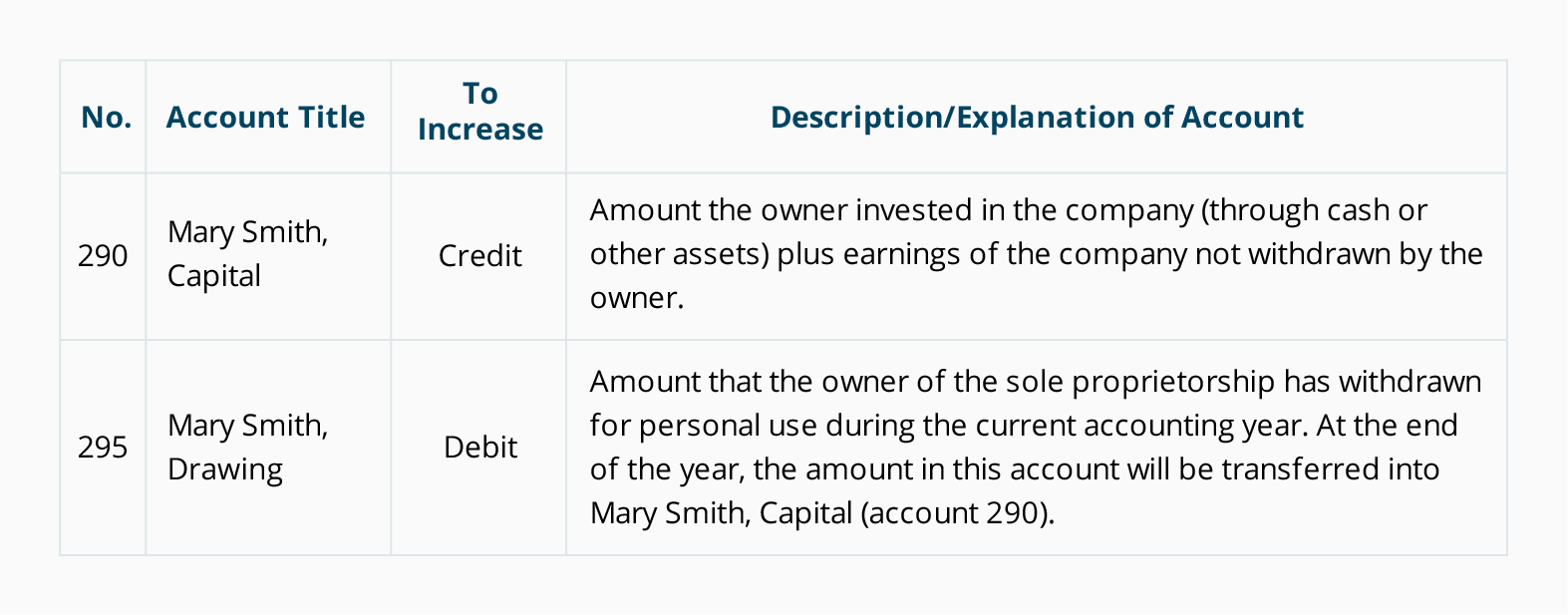

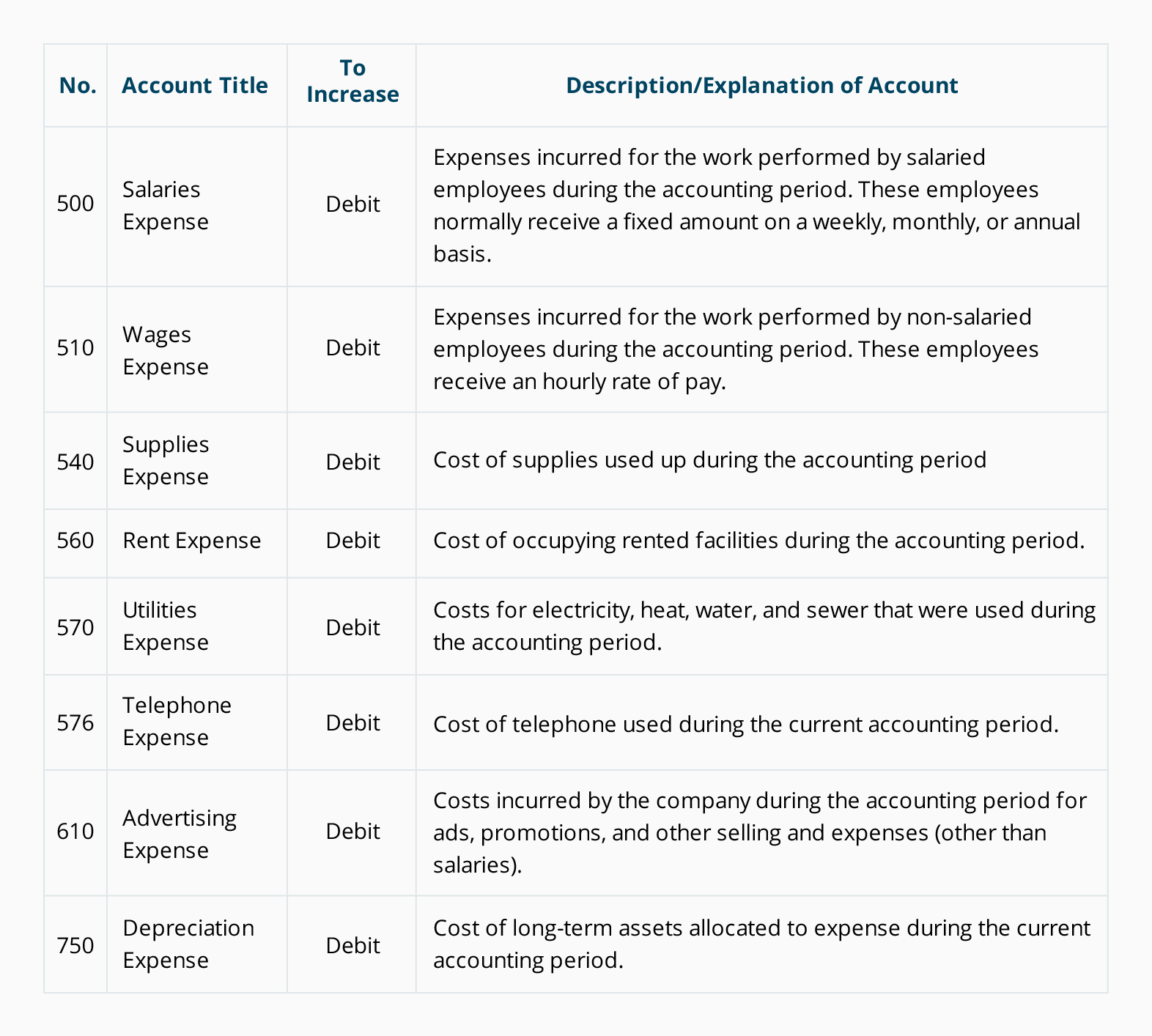

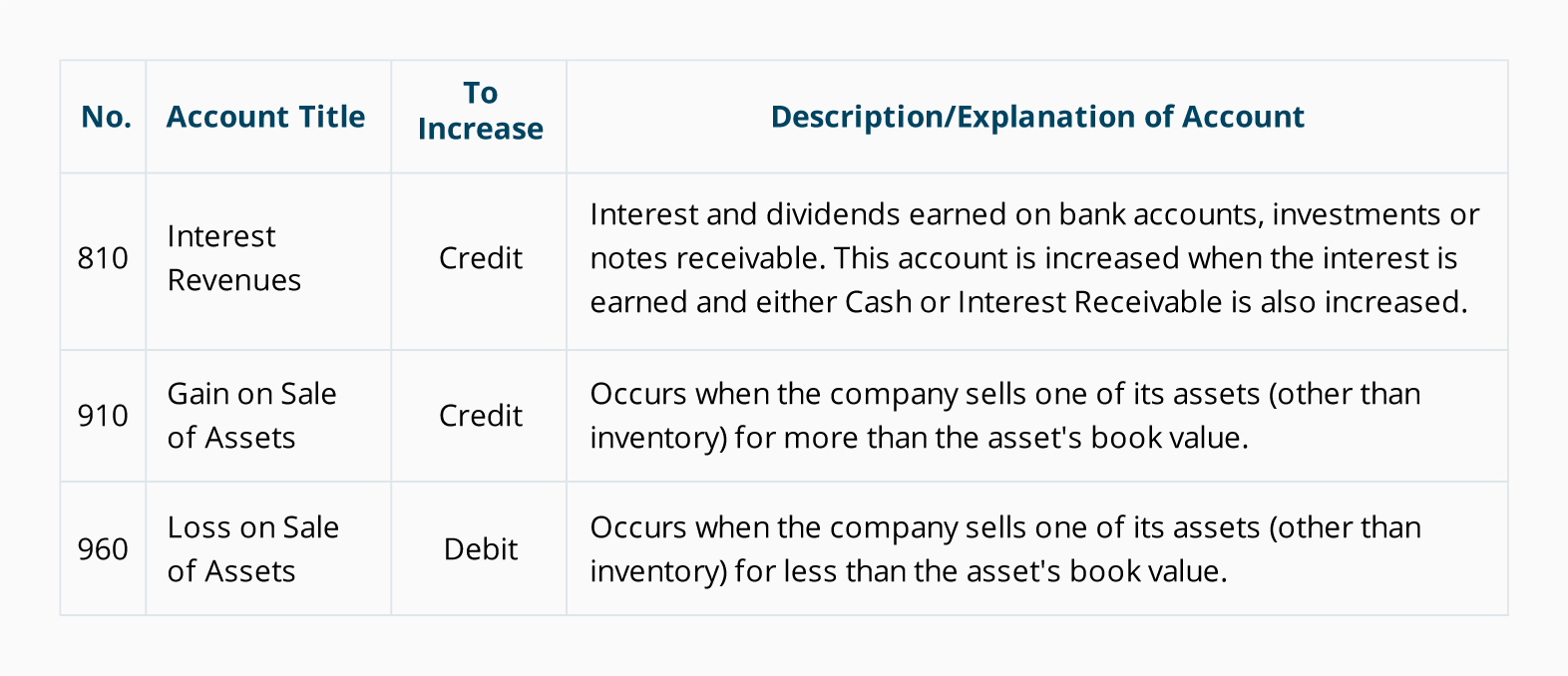

This is a partial listing of another sample chart of accounts. Note that each account is assigned a three-digit number followed by the account name. The first digit of the number signifies if it is an asset, liability, etc. For example, if the first digit is a “1” it is an asset, if the first digit is a “3” it is a revenue account, etc. The company decided to include a column to indicate whether a debit or credit will increase the amount in the account. This sample chart of accounts also includes a column containing a description of each account in order to assist in the selection of the most appropriate account.

Asset Accounts

Liability Accounts

Owner’s Equity Accounts

Operating Revenue Accounts

Operating Expense Accounts

Non-Operating Revenues and Expenses, Gains, and Losses

Accounting software frequently includes sample charts of accounts for various types of businesses. It is expected that a company will expand and/or modify these sample charts of accounts so that the specific needs of the company are met. Once a business is up and running and transactions are routinely being recorded, the company may add more accounts or delete accounts that are never used.

At Least Two Accounts for Every Transaction

The chart of accounts lists the accounts that are available for recording transactions. In keeping with thedouble-entry system of accounting, a minimum of two accounts is needed for every transaction—at least one account is debited and at least one account is credited.

When a transaction is entered into a company’s accounting software, it is common for the software to prompt for only one account name—this is because the software is programmed to automatically assign one of the accounts. For example, when using accounting software to write a check, the software automatically reduces the asset account Cash and prompts you to designate the other account(s) such as Rent Expense,Advertising Expense, etc.

Some general rules about debiting and crediting the accounts are:

- Expense accounts are debited and have debit balances

- Revenue accounts are credited and have credit balances

- Asset accounts normally have debit balances

- To increase an asset account, debit the account

- To decrease an asset account, credit the account

- Liability accounts normally have credit balances

- To increase a liability account, credit the account

- To decrease a liability account, debit the account